Fishing Trip Insurance Explained: Protect Your Gear

TL;DR:

- Standard travel insurance often excludes fishing activities, requiring specialized coverage for anglers.

- Fishing trip insurance covers trip disruptions, gear loss, medical emergencies, and remote rescue costs.

- Buying insurance early, within 14-21 days of deposit, ensures better coverage options and claim support.

Most anglers spend months planning a fishing trip, investing thousands in gear, guides, and flights, then hand everything over to a standard travel policy that quietly excludes the activities they came for. Standard travel insurance often excludes deep-sea fishing and remote-area excursions, classifying them as adventure sports requiring specialist coverage. That single oversight can leave you paying out of pocket for lost rods, canceled charters, or a medical evacuation miles offshore. This guide explains what fishing trip insurance actually covers, how it differs from ordinary travel policies, what it costs, and how to file a claim without getting burned.

Table of Contents

- What is fishing trip insurance?

- Key coverages and exclusions: What anglers should know

- Insuring your gear: How much protection do you need?

- Costs and buying tips: Making the most of your policy

- How to file a claim and common pitfalls

- Our take: What most anglers miss about fishing trip insurance

- Ready to protect your next fishing adventure?

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Specialized protection needed | Standard travel insurance rarely provides enough coverage for anglers, so seek a policy tailored to fishing trips. |

| Cover gear and emergencies | Fishing trip insurance protects not just your travel investment, but also valuable equipment and medical emergencies. |

| Buy early for full benefits | Purchase your policy soon after booking to maximize your options, including cancellation waivers and broader coverage. |

| Understand exclusions | Know what’s not covered—like certain gear wear or boat issues—to avoid claim surprises. |

| Document for claims success | Thoroughly document your equipment and trip details to streamline the claims process and avoid denials. |

What is fishing trip insurance?

Fishing trip insurance is not simply travel insurance with a fishing logo on the brochure. It is a category of coverage built specifically around the risks anglers face, from weather-forced cancellations to a reel falling overboard in open water.

Fishing trip insurance is a specialized form of adventure travel insurance designed for anglers on fishing excursions, covering trip disruptions, medical emergencies, gear loss, and activity-specific risks not included in standard policies. That distinction matters more than most people realize.

A standard travel policy typically covers flight delays, lost luggage, and basic medical care. It is built for someone catching a connecting flight in Frankfurt, not someone catching marlin sixty miles off the coast of the Maldives. When fishing is listed at all, it is usually buried under a blanket adventure sports exclusion.

Here is what a specialist fishing policy usually protects:

- Trip cancellation and interruption caused by weather, illness, or guide unavailability

- Emergency medical coverage including evacuation from remote fishing grounds

- Gear and equipment loss covering rods, reels, electronics, and tackle

- Weather-related disruptions when your charter cannot legally depart

- Government-imposed fishing restrictions that shut down your planned destination

- Search and rescue costs if you end up in trouble far from shore

“Standard travel insurance is designed for sightseers, not anglers. If your trip centers on fishing, your insurance should too.”

Anyone planning to book through JustFishing Group and head out to destinations like Socotra, Kenya, or the Seychelles is fishing in remote, sometimes unpredictable environments. A generic policy built for beach holidays will not account for those realities. Checking the fishing policy details on a specialist provider before you book is the single smartest pre-trip move you can make.

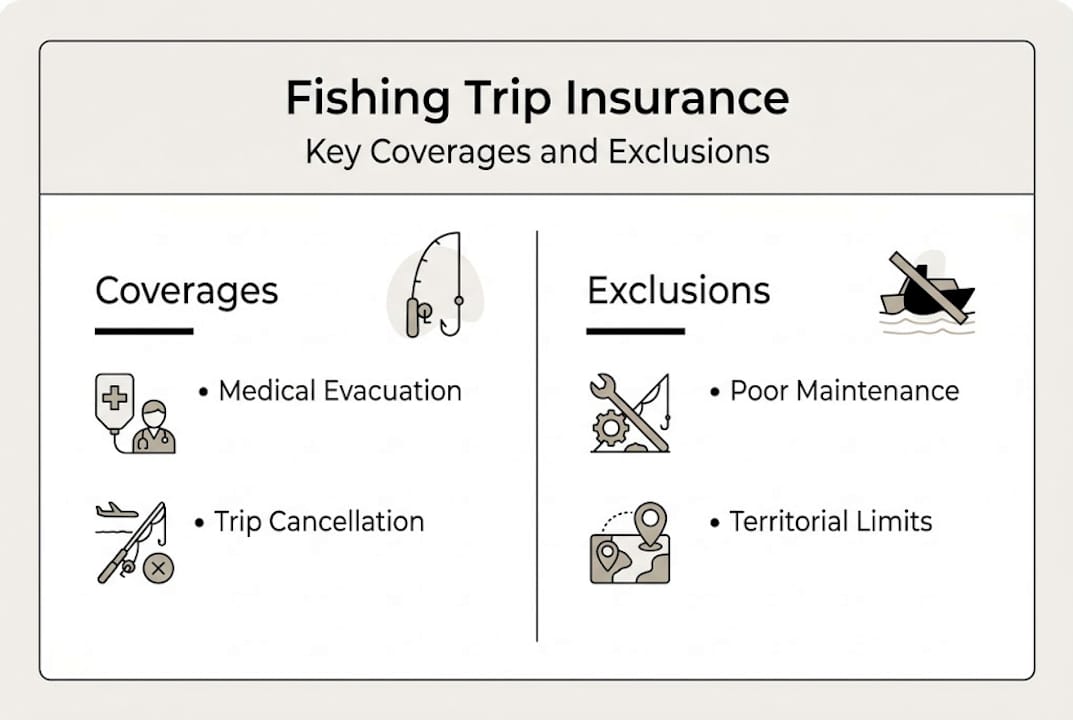

Key coverages and exclusions: What anglers should know

Knowing what a policy can cover is only half the picture. Understanding what it specifically excludes is often what separates a useful policy from an expensive disappointment.

What specialist policies typically include:

Common coverages include emergency medical and evacuation up to £10 million, trip cancellation and interruption, baggage and gear loss for rods and reels up to £2,500 to £10,000 depending on the plan, weather disruptions, search and rescue, and government fishing restrictions. That is a meaningfully broader safety net than anything a standard policy offers.

| Coverage type | Specialist fishing policy | Standard travel policy |

|---|---|---|

| Emergency medical and evacuation | Yes, including offshore | Basic, often excludes remote areas |

| Gear and tackle loss | Yes, specific sublimits | Rarely, or very low limits |

| Trip cancellation (weather) | Yes | Sometimes, limited conditions |

| Search and rescue | Yes | Usually excluded |

| Fishing activity coverage | Yes | Often excluded as adventure sport |

| Government fishing restrictions | Yes | No |

Common exclusions you need to know:

- Pre-existing medical conditions unless you purchase a waiver

- Gear damage from normal wear and tear

- High-risk activities not specifically listed in the policy

- Known weather events at the time of purchase

- Fishing in restricted or unlicensed territory

About 30% of boat-related claims are denied due to maintenance issues or territorial violations. That is a significant number, and it catches anglers off guard every season.

Pro Tip: Read the activity schedule in your policy, not just the summary. The activity schedule is the actual legal list of what is covered. If “deep-sea fishing” or “offshore fishing” is not explicitly named there, assume it is excluded.

If you regularly book deep-sea fishing trips to open-water destinations, always confirm that your specific trip type is named in the coverage schedule before you pay your deposit.

Insuring your gear: How much protection do you need?

Your rod, reel, sonar unit, and tackle bag can easily add up to several thousand dollars. For many anglers, the gear costs more than the flights. So it is worth understanding exactly how insurance handles it.

Standard travel policies apply sublimits to valuables, which means even if the total payout cap is generous, your fishing equipment may be covered only up to a fraction of its real value. Specialist policies raise those sublimits considerably, but you still need to check the numbers against your actual gear value.

Here is a realistic example of how a claim plays out:

| Item | Actual value | Policy sublimit | Out-of-pocket loss |

|---|---|---|---|

| High-end rod and reel combo | $3,200 | $1,500 | $1,700 |

| Marine electronics (sonar/GPS) | $4,100 | $1,000 | $3,100 |

| Tackle and accessories | $1,800 | — | $1,800 |

| Total | $9,100 | $2,500 | $6,600 |

One real claim example involved an angler who lost $9,100 in gear and electronics; the standard $2,500 sublimit was paid, leaving $6,600 out of pocket. That gap is not a technicality. It is a budget-destroying reality.

Here is what you should do before buying any policy:

- Inventory every item you are traveling with and assign a current replacement value

- Compare your total gear value to the policy sublimit, not the total coverage cap

- Look for specialist policies that offer itemized coverage for high-value items

- Keep purchase receipts and photos of your gear before you travel

Pro Tip: Photograph your gear laid out before every trip and timestamp the photos. If you need to file a claim, visual proof of condition and quantity speeds up the process significantly.

Whether you travel with premium fishing gear brands or pack a lure bag full of hand-tied flies, protecting what you bring is worth the extra effort. Even a quality tackle box stocked with upgraded tackle accessories can represent a significant insurable value.

Costs and buying tips: Making the most of your policy

The price of fishing trip insurance surprises most people, and not always in the direction they expect. It is usually more affordable than anglers assume, but only when purchased at the right time.

Fishing trip insurance typically costs 4 to 10% of your total trip cost, meaning a $3,500 fishing trip would cost between $140 and $350 to insure fully. For that price, you get coverage that a standard policy simply cannot match.

Timing is where most people lose out. Buying within 14 to 21 days of your initial trip deposit is the window that unlocks two critical benefits: Cancel For Any Reason (CFAR) coverage and pre-existing medical condition waivers. Miss that window, and those options are gone, regardless of how much you are willing to pay later.

Statistic to remember: Adventure plans average $30 per day, and comparison platforms like Squaremouth let you filter 30 or more providers specifically for fishing and water sports coverage. That kind of side-by-side view saves both time and money.

Here is a step-by-step approach to buying the right policy:

- Calculate your total trip cost including flights, lodging, guide fees, and gear value

- Set a purchase deadline at 14 days after your first deposit payment

- Use a comparison platform to filter specifically for water sports and fishing activity coverage

- Check the activity schedule to confirm your specific type of fishing is covered

- Add CFAR if your trip is expensive or involves non-refundable bookings

- Read the exclusions section before finalizing any purchase

For practical guides on trip planning and safety, the JustFishing blogs regularly cover destination-specific risks worth reviewing before you insure.

How to file a claim and common pitfalls

Buying the right policy is step one. Knowing how to actually use it when something goes wrong is what determines whether you get paid.

The claims process is more documentation-heavy than most anglers expect. Insurance companies do not take your word for it. They want receipts, reports, photos, and timelines.

Here is how to approach it correctly:

- Report the incident immediately. Most policies require notification within 24 to 72 hours of any covered event.

- Get a written report. For theft or gear loss, file a local police report. For medical events, get hospital documentation.

- Photograph everything. Damaged gear, weather conditions, the location. More evidence is always better.

- Keep all receipts. Charter cancellation fees, alternative accommodation, medical costs.

- Submit within the policy deadline. Claims submitted late are frequently denied regardless of validity.

- Follow up in writing. Phone calls are easy to dismiss. Email creates a paper trail.

“Growing demand from rising angling participation has increased claims complexity, particularly around weather and gear wear disputes.”

The most common denial reasons come down to documentation gaps and timing failures, not fraudulent claims. Gear wear is also a frequent gray area. An insurer can deny a rod replacement claim if there is evidence of prior damage or poor maintenance, so keeping your equipment in documented good condition matters.

Some anglers report that claim advocacy from comparison platforms helps when disputes arise, but the best defense is always a thorough paper trail from the moment something goes wrong.

Our take: What most anglers miss about fishing trip insurance

Here is the honest truth we keep seeing: anglers who travel with gear worth $5,000 or more routinely insure it with policies designed for someone bringing a carry-on bag to a resort. The mismatch is almost comical until someone loses their setup overboard.

Specialist trip insurance is not a luxury reserved for professional tournament anglers. If you are traveling internationally with quality gear and non-refundable bookings, you are already in the category of angler who needs it. The conversation should not be “do I really need this?” It should be “which policy actually fits my trip?”

The other mistake we see constantly is buying insurance after a problem appears. The moment a storm is named or a health issue surfaces, your coverage options shrink dramatically. Proactive planning, buying early and buying right, is the actual protection. Cheap insurance bought at the last minute is mostly paperwork.

If you want trips where risks are already well-considered, explore tailored fishing adventures built for real angling conditions worldwide.

Ready to protect your next fishing adventure?

You’ve spent real money planning your trip and packing your gear. The last thing you want is an unexpected cancellation, a stolen rod, or a weather shutdown leaving you with nothing to show for it.

At JustFishing Group, we pair curated fishing trip packages across world-class destinations with the kind of gear worth protecting. From the Maldives to Morocco, every trip we offer is designed for serious anglers. Before you head out, make sure your equipment travels safely too. Explore options to secure your gear and browse trips that match your ambition. Your next great fishing story deserves the best possible start.

Frequently asked questions

What does fishing trip insurance usually cover?

Fishing trip insurance covers trip disruptions, medical emergencies, gear loss, weather cancellations, and activity-specific risks not included in standard travel insurance.

Is fishing considered an adventure sport for insurance purposes?

Yes, most insurers classify fishing, especially deep-sea or remote trips, as an adventure sport, which means basic travel policies routinely exclude it from coverage.

How much does fishing trip insurance cost?

It typically costs 4 to 10% of your total trip cost, which works out to roughly $140 to $350 for a $3,500 trip.

When should I buy fishing trip insurance for the best coverage?

Purchase within 14 to 21 days of your initial deposit to qualify for Cancel For Any Reason coverage and pre-existing medical condition waivers.